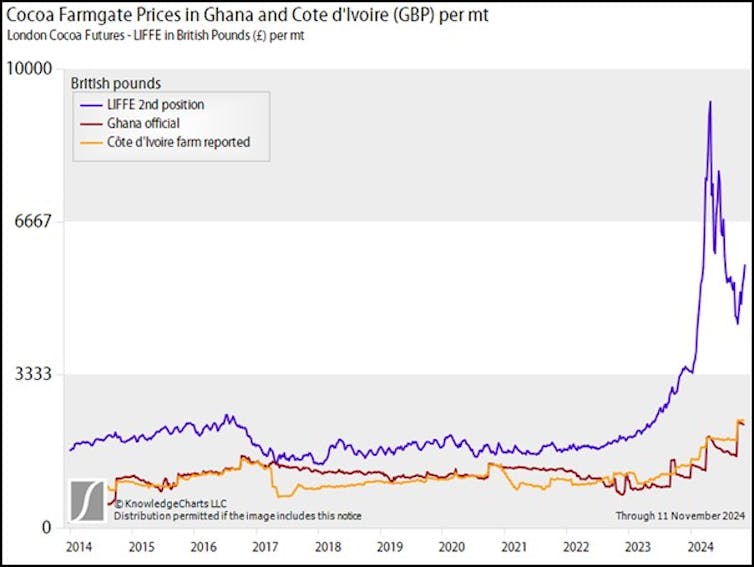

International cocoa prices have experienced a historic price surge, rising by over 300% in the space of 12 months from £2,166 per tonne of cocoa in April 2023 to £9,980 by April 2024. Prices have fallen since then, and are currently hovering around the £6,400 mark at the time of writing.

This rally, which is the highest on record for cocoa, was driven by poor harvests in the Ivory Coast and Ghana. Powerful El Niño weather events, coupled with years of underinvestment that left Ghana’s cocoa trees vulnerable to diseases, have decimated yields.

In February 2024 Ghana’s cocoa board, Cocobod, revised its cocoa crop forecast down 40% from its initial target of 820,000 metric tonnes for the 2023–24 season. Ghana and the Ivory Coast account for nearly 60% of global cocoa production, so markets reacted to the news swiftly.

We are researchers of the global cocoa trade, and one of us is particularly familiar with the mechanics of Ghana’s cocoa sector. Fuad is currently the head of the Ghana Cocoa Marketing Company UK, which facilitates trade transactions between the Cocoa Marketing Company Ghana (CMC) – a subsidiary of Cocobod and the monopoly seller of Ghanaian cocoa beans – and its clients across the world.

The tripling of cocoa prices in London, which serve as the benchmark for west African cocoa, should have been a blessing for Ghana’s economy and its cocoa farmers, many of whom have long struggled with low incomes. However, the prices farmers are paid for their cocoa (farmgate prices) remained well below international market prices despite the extraordinary surge.

Cocobod increased farmgate prices by 58% in April, followed by another 45% hike at the start of the 2024–25 season in September. This latter move increased the price farmers are paid per tonne of cocoa from 33,120 Ghanaian cedis (£1,599) to 48,000 Ghanaian cedis (£2,304).

A further 3.3% price increase was announced by Ghana’s president, Nana Akufo-Addo, during the celebration of Ghana’s National Farmer’s Day on November 8 in a bid to motivate cocoa farmers.

These price hikes are significant, but they have not kept pace with the movement in the global benchmark. This has led to a growing gap between farmgate prices in Ghana and the Ivory Coast, and the international market.

Locking prices in early

In our recent working paper, we show that the limited pass-through of global prices to farmers in Ghana was primarily due to the combined effect of a longstanding forward sales strategy and a financing structure that relies on a loan sourced from a group of international banks (a syndicated loan).

For decades, the CMC has used forward sales to hedge against downward trending prices. This involves selling up to 70% of the anticipated cocoa crop between nine and 12 months ahead of harvest to international traders and local processors at prices tied to the global benchmark.

The average price secured through these contracts is then used to set farmgate prices before the start of each cocoa season. This system protects farmers from price drops in a declining market, but it does not allow them to benefit if the spot price at harvest is above the forward price that is achieved by the CMC.

With a near-tripling of cocoa prices in only 12 months, the average forward prices secured by the CMC were significantly lower than the levels achieved in international spot markets. This limited the potential for a substantial increase in farmgate prices.

Besides price risk management, the forward sales fulfil another role. For over 31 years, Cocobod has relied on a syndicated loan to finance the purchase of cocoa beans from farmers, as well as farming inputs such as fertilisers and jute bags. The forward contracts are used as collateral against which the loan is drawn.

Cocobod has raised nearly US$28 billion (£21.6 billion) through the loan since its inception. Given the size of the cocoa sector in the overall economy – cocoa has ranked consistently among Ghana’s top four exports over the past three decades – the loan’s importance goes beyond the cocoa trade.

The loan has provided the Ghanaian central bank with the ability to borrow hard currency at affordable interest rates. Hard currency is needed to pay for imports and to stock up on foreign exchange reserves. This is particularly needed now as Ghana’s debt crisis has made other means of external borrowing more challenging since 2021.

Because of the need for collateral to secure the loan, forward contracts must be signed and prices locked in before the season starts. This limits the volume of cocoa that can be sold at a more favourable spot price when market conditions improve.

Breaking free

A downward trending cocoa price over the longer term remains a concern. But extreme weather caused by climate change, and the resulting increased market volatility, have put into question the sustainability of both the forward sales system and the loan.

So, in August 2024 the chief executive of Cocobod, Joseph Boahen Aidoo, announced that Ghana would not raise a loan for the 2024–25 season. The decision to end three decades of dependency on this financing model was made in light of significantly higher interest rates, which has made offshore borrowing much less attractive.

Cocobod’s new financing model requires licensed buying companies (LBCs), which are responsible for purchasing cocoa beans from farmers at the price set by Cocobod, to secure funding independently. Previously, they received centralised funding from Cocobod through the loan.

Under this new system, LBCs primarily source funding from international cocoa traders and, to a lesser extent, domestic banks. The LBCs buy cocoa from farmers with the secured funding and deliver it to the CMC. They are then reimbursed for the amount they paid farmers for the beans plus an agreed margin for their service by Cocobod.

However, the need for LBCs to secure their own financing within a short planning window poses challenges for some in the 2024–25 season, particularly as local firms face hurdles in accessing affordable domestic credit. In an effort to ensure sufficient volumes, many international traders have established sourcing partnerships with local buyers. But some local buyers argue that this could further consolidate power among multinational firms because the buyers would essentially become beholden to them.

Ghana’s 31-year reliance on the cocoa-backed loan has constrained its ability to fully capitalise on price rallies. The shift to a new financing model grants the CMC flexibility to time its cocoa sales, utilising both forward and spot contracts. It also has the potential to improve cash liquidity for Ghana’s cocoa buying companies.

With proper execution and commitment by Cocobod to ensure timely reimbursement, this approach could reshape Ghana’s cocoa industry and significantly improve the livelihoods of nearly 1 million cocoa farming families.

Source: the conversation

{kind=link}